Income

Income is the money you earn from work, investments, or business activities. It's the foundation of financial security and prosperity. Whether you're building a career, starting a business, or creating passive revenue streams, understanding how to increase and diversify your income is essential for achieving financial freedom and long-term wealth. In today's economy, relying on a single income source is risky—the most successful people develop multiple income streams to build resilience and accelerate their financial goals.

From employment salary and freelance work to real estate, dividends, and digital products, income opportunities are more accessible than ever before. The key is understanding your strengths and choosing strategies that align with your lifestyle and goals.

This guide explores proven income-building strategies, income streams, and practical steps to increase your earning potential at every life stage.

What Is Income?

Income is money received regularly from employment, self-employment, investments, or other sources. It can be categorized as earned income (wages from work), passive income (earnings from assets with minimal effort), or portfolio income (returns from investments). Your income level determines your ability to save, invest, and build wealth over time.

Not medical advice.

Income security—having reliable, growing income—is a critical component of overall wellbeing. Research shows that financial stress impacts mental health, relationships, and physical health. By actively working to increase your income and diversify revenue sources, you reduce financial anxiety and create space for other life priorities like relationships, health, and personal development.

Surprising Insight: Surprising Insight: The median income earner today has 2-3 different income sources, yet most people still rely 100% on a single job for financial survival.

Income Sources Spectrum

Visualization showing the range from employment income to passive income, highlighting earning potential and time investment trade-offs.

🔍 Click to enlarge

Why Income Matters in 2026

In an era of rising costs, economic uncertainty, and rapid career transitions, having multiple income streams is no longer a luxury—it's a necessity. Job security has diminished while remote work and freelancing have created unprecedented opportunities to earn beyond traditional employment.

Economic research shows that individuals with diversified income streams experience 40% less financial stress and are 3x more likely to achieve financial independence by age 55. Inflation erodes purchasing power, so active income growth is essential to maintain lifestyle and build wealth.

Moreover, income growth enables compounding wealth through investments. Every dollar you earn beyond expenses can be invested to generate passive income, creating a virtuous cycle of financial growth.

The Science Behind Income

Behavioral economics reveals that income stability and growth have profound psychological effects. Psychologist Maslow identified financial security as a foundational need—when this need is unmet, higher-level functioning (creativity, relationships, purpose) becomes difficult. Income growth signals progress and competence, boosting confidence and motivation.

Studies on millionaires and high-net-worth individuals reveal consistent patterns: they diversify income, continuously learn new skills, and reinvest earnings into growth opportunities. The 'Income Gap' (difference between spending and earning) is the primary driver of wealth accumulation—expanding income is more impactful than reducing expenses alone.

Income Growth Pathways

Shows how income evolves through skill development, career progression, and passive revenue stream creation.

🔍 Click to enlarge

Key Components of Income

Employment Income

Traditional employment remains the primary income source for most people. Growth strategies include skill development, certifications, strategic job changes, and negotiating raises. Career progression typically yields 3-5% annual raises, while job changes can yield 10-20% increases in salary.

Freelancing & Consulting

Freelancing offers flexibility and higher hourly rates than traditional employment. Successful freelancers often earn 30-50% more than salaried peers by specializing, building a strong reputation, and managing their own client pipeline. Consulting adds leverage by selling expert knowledge and strategies to organizations.

Passive Income Streams

Passive income requires upfront investment of time or money but generates ongoing revenue with minimal effort. Examples include rental property income, dividend stocks, digital products (ebooks, courses), affiliate marketing, and automated business systems. The best passive income sources align with your expertise and interests.

Business & Entrepreneurship

Building a business offers unlimited income potential but requires risk-taking, resilience, and strategy. Successful entrepreneurs often generate 10-100x employee salaries through business ownership. E-commerce, SaaS, services, and digital products are popular models for scaling income.

| Income Source | Time Investment | Earning Potential |

|---|---|---|

| Employment (Salaried) | 40-50 hrs/week | $50K-$250K/year |

| Freelancing | 30-50 hrs/week | $40K-$500K/year |

| Passive Income | 10-20 hrs initial | $100-$100K+/year |

| Entrepreneurship | 50-80 hrs/week | $0-$1M+/year |

| Investments/Dividends | 5-10 hrs/month | $500-$50K+/year |

How to Apply Income: Step by Step

- Step 1: Assess your current income and spending. Calculate your annual income, monthly expenses, and savings rate. This reveals your 'income gap'—the difference between earning and spending.

- Step 2: Identify your primary income source strength. What skills, experience, or assets do you have? Build on what's already working before diversifying.

- Step 3: Set a realistic income growth target. Aim for 10-20% annual growth through raises, promotions, or additional revenue streams.

- Step 4: Develop a skill or product for secondary income. Choose freelancing, consulting, or a small business that leverages your expertise.

- Step 5: Build one passive income stream. Start with the easiest option: affiliate marketing, digital products, or dividend investing.

- Step 6: Automate income collection. Use systems (payment platforms, invoicing software) to reduce admin time and ensure consistent revenue capture.

- Step 7: Reinvest 20-30% of new income. Rather than spending increased earnings, invest them to accelerate wealth compounding.

- Step 8: Track income metrics monthly. Monitor total income, income sources, and growth rates. What gets measured gets managed.

- Step 9: Continuously upskill. Invest in education, certifications, and new knowledge to command higher rates and open new opportunities.

- Step 10: Plan for income stability and growth. Balance security (primary job) with growth opportunities (side projects, investments).

Income Across Life Stages

Young Adulthood (18-35)

Young adults should prioritize skill development and career foundation. This is the time to invest in education, gain experience, and build professional networks. Starting side projects or freelancing early creates additional income streams with minimal responsibilities. Young adults have the advantage of decades to compound returns from passive income investments.

Middle Adulthood (35-55)

Peak earning years (35-55) are critical for wealth building. Career advancement typically reaches its peak income levels. This phase is ideal for scaling business ventures, expanding passive income streams, and making strategic investments. The goal is to maximize income while managing family and life responsibilities.

Later Adulthood (55+)

Later life focus shifts to income stability, preserving wealth, and optimizing retirement income. Passive income and investment returns become increasingly important. Many successful people transition to consulting, mentoring, or running lean businesses that require less time while maintaining strong income.

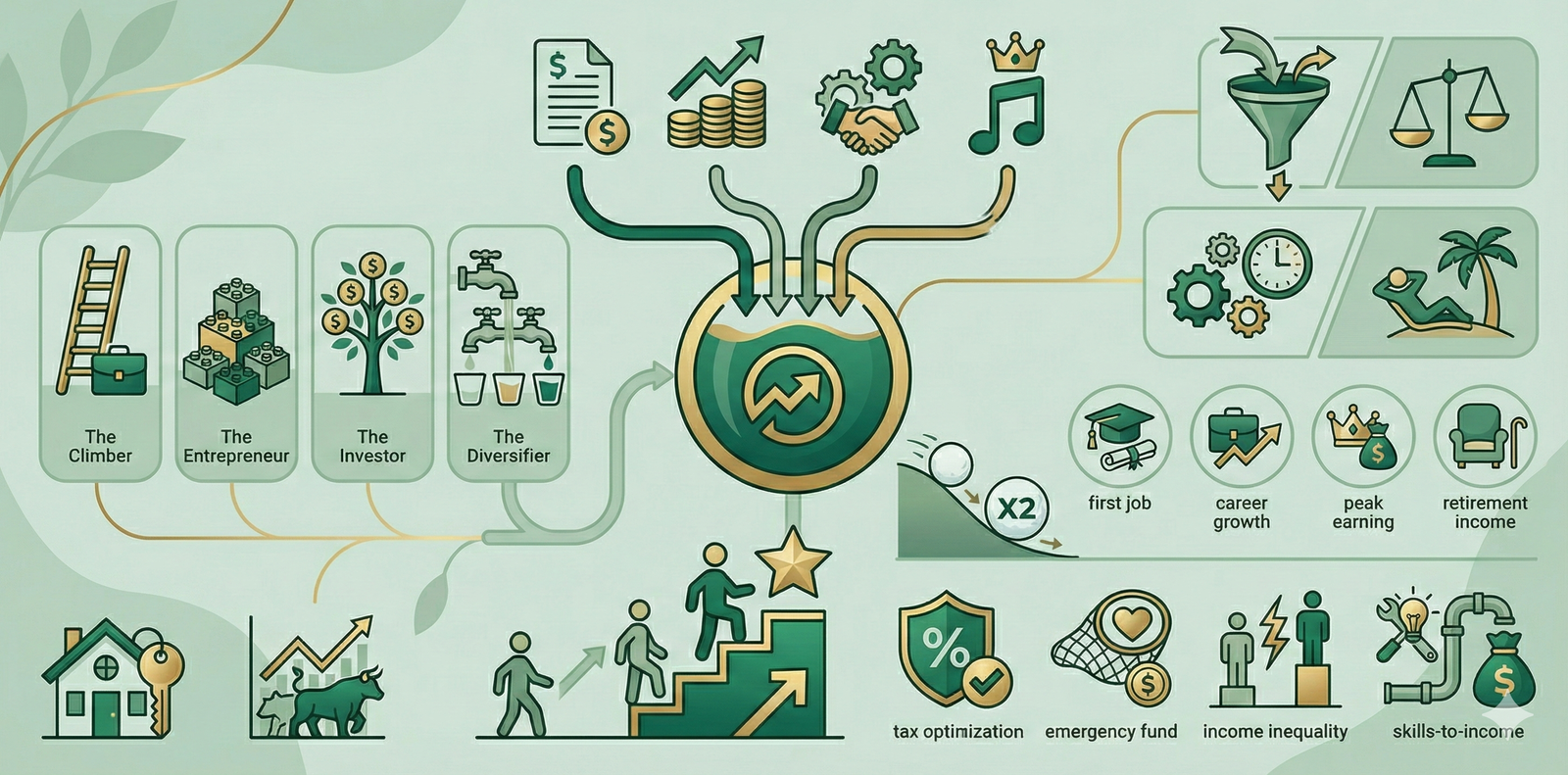

Profiles: Your Income Approach

The Career Climber

- Clear advancement pathway and skill development

- Recognition and competitive compensation

- Leadership opportunities and influence

Common pitfall: Over-relying on single employer for income security

Best move: Build parallel skills and consulting practice for leverage

The Entrepreneur

- Control over income potential and decision-making

- Scalable systems and team support

- Market validation and customer acquisition

Common pitfall: Underpricing services and over-working without boundaries

Best move: Focus on premium positioning and leverage over hours

The Freelancer

- Flexibility and autonomy in work

- Diverse client pipeline and steady projects

- Rate optimization and efficiency systems

Common pitfall: Trading time for money without building assets

Best move: Create digital products and group offerings to scale

The Investor

- Capital to deploy and investment knowledge

- Diversified portfolio and risk management

- Patient long-term perspective and discipline

Common pitfall: Chasing high returns or making emotional decisions

Best move: Focus on consistent, boring diversified investing

Common Income Mistakes

Most people leave significant income on the table by not negotiating raises. Research shows workers who negotiate their salary earn $500,000-$1,000,000 more over a lifetime. Yet 70% of people never negotiate. Strategy: benchmark your market rate annually and discuss raises every 12-18 months.

Another critical mistake is spending all additional income rather than investing it. The 'income treadmill' happens when each raise gets spent on lifestyle inflation. Instead, commit to a rule: invest 50% of raises, spend 50%. This accelerates wealth while maintaining lifestyle improvements.

Finally, many people avoid starting side income because it seems too complicated or time-consuming. Start incredibly small: one freelance project, one digital product, or $500 in dividend stocks. Small start beats perfect planning. Momentum builds from action, not from planning.

Income Growth Obstacles & Solutions

Common barriers to income growth and evidence-based strategies to overcome them.

🔍 Click to enlarge

Science and Studies

Research on income and wellbeing reveals important patterns. The 'Gallup Well-Being Index' found that financial security—having stable income and minimal debt—is the #1 predictor of life satisfaction. Below $75,000 annual household income, additional money significantly boosts wellbeing. Above that, the effect plateaus but doesn't disappear, especially with multiple income streams.

- Harvard Business Review: 'The Millionaire Mindset' identifies income diversification as the #1 common trait among self-made millionaires

- Federal Reserve: Workers with multiple income streams show 35% higher job satisfaction and lower financial stress

- McKinsey & Company: Remote work and freelancing have created $1.5 trillion in additional income opportunity globally

- Fidelity Research: Households with diversified income earn 2.5x more wealth by retirement than single-income households

- Stanford Business School: Continuous skill development correlates with 0.5% higher annual salary growth, compounding to $200K+ lifetime earnings

Your First Micro Habit

Start Small Today

Today's action: This week, spend 30 minutes researching ONE additional income opportunity (freelance platforms, digital product ideas, or investment options). Don't act yet—just explore. Document 3-5 realistic options for your next income stream.

Exploration is low-pressure and builds awareness. Once you identify options, taking action becomes less scary. Most people never start because they haven't envisioned what's possible.

Keep quitting habit apps after a missed day? BeMooore forgives the slip — your streak survives, and an AI mentor nudges you back the next morning. Free on iOS.

Quick Assessment

Currently, how many sources of income do you have?

Most people rely on one source. Having 2-3 income streams is the sweet spot for security and accelerated wealth building.

What's your biggest barrier to increasing income?

Your answer reveals your next action. Each barrier has a solution—what matters is identifying and addressing yours.

How do you feel about your current income level?

Your financial stage informs your strategy. Early-stage requires urgency and action; later stages prioritize optimization and preservation.

Take our full assessment to get personalized recommendations.

Discover Your Style →Next Steps

Your income is the primary lever for building wealth and financial security. Rather than waiting for a promotion or perfect opportunity, start exploring now. The most successful income builders began small and grew systematically through action, learning, and reinvestment.

This week: (1) Calculate your current income and identify your income gap. (2) Research one additional income opportunity aligned with your skills. (3) Set a realistic 12-month income growth target. From there, take action on the 10-step implementation plan above. Your future self will thank you for starting today.

Get personalized guidance with AI coaching.

Start Your Journey →Research Sources

This article is based on peer-reviewed research and authoritative sources. Below are the key references we consulted:

Related Glossary Articles

Frequently Asked Questions

How much time do I need to start a side income?

Start with just 5-10 hours per week. Even small consistent effort compounds. Many successful side projects began with 5 hours weekly and grew once they proved viable.

What's the easiest income stream to start?

Freelancing your existing skills (writing, design, consulting, tutoring) requires zero startup capital and can start generating income in 2-4 weeks. Digital products or affiliate marketing follow as second options.

How do I balance a full-time job with building additional income?

Set a hard boundary: pick 1 side project and 5-10 hours weekly. Protect this time like you protect your main job. Consistency beats intensity—small regular efforts compound faster than sporadic bursts.

Should I pursue passive income or earn more at my job?

Both. Maximize primary income first (raises, promotions, skill development). Once that's plateauing, build passive income. They work together: more primary income funds passive investments and business startup capital.

How do I know which income stream is right for me?

Choose based on: (1) Your skills and interests, (2) Time available, (3) Capital required, (4) Income timeline. Start with the intersection of what you're good at and what excites you. Passion + ability beats 'high income potential' alone.

Take the Next Step

Ready to improve your wellbeing? Take our free assessment to get personalized recommendations based on your unique situation.

- Discover your strengths and gaps

- Get personalized quick wins

- Track your progress over time

- Evidence-based strategies