Retirement

Retirement represents one of life's most significant transitions—the culmination of decades of work transformed into years of freedom. Whether you envision quiet mornings without alarm clocks, travel to dream destinations, or pursuing passions long deferred, retirement promises a fresh chapter. Yet this freedom comes with a crucial reality: you must strategically build and protect the financial foundation that makes it possible. The difference between a retirement filled with possibility and one marked by financial stress often comes down to decisions made years—sometimes decades—in advance. This guide explores how to navigate every dimension of retirement, from practical savings strategies to the psychological transition that awaits, ensuring your dream of financial freedom becomes your lived reality.

Today, traditional full retirement at 65 is just one option among many. Some people retire in their 40s through strategic investments, while others discover meaning in working longer with greater flexibility. Social Security provides a foundation, but most people need to build substantial savings beyond government programs. The challenge isn't complexity—it's clarity about what you want and commitment to planning for it.

Modern retirement planning involves understanding tax-advantaged accounts, withdrawal strategies that sustain your wealth, healthcare coverage before Medicare, and the emotional preparation that transforms retired identity into lived reality.

What Is Retirement?

Retirement is a life stage when you stop full-time employment and rely primarily on savings, investments, pensions, and government benefits rather than a paycheck. More broadly, it's the transition from work-centered identity to self-directed living where you design your days according to your values, interests, and relationships rather than employment obligations.

Not medical advice.

Traditional retirement—leaving the workforce completely at a set age—is evolving. Today's retirement landscape includes phased retirement (gradually reducing work), semi-retirement or 'BaristaFIRE' (part-time work plus savings), and complete early retirement achieved through aggressive saving. The only requirement is that your income sources (savings, investments, Social Security) exceed your living expenses without active employment.

Surprising Insight: Surprising Insight: The average healthy 65-year-old couple will need $17,000+ annually just for healthcare costs in early retirement, rising to over $55,000 by age 85—money many people never account for in their retirement plans.

Retirement Income Sources Breakdown

Visual showing typical retirement income composition: Social Security, pensions, investments, and part-time work

🔍 Click to enlarge

Why Retirement Matters in 2026

In 2026, retirement planning faces unprecedented challenges and opportunities. Social Security recipients received a 2.8% benefit increase, with average monthly payments rising to approximately $2,071, but Medicare Part B premiums jumped 9.7% to $202.90 monthly—a pattern likely to continue. Healthcare inflation consistently outpaces Social Security benefits, meaning retirees face declining purchasing power for their largest expense category unless they've built substantial savings.

The traditional 4% withdrawal rule—once gospel for retirement planning—is losing credibility among experts who recognize that fixed-rate withdrawals fail under volatile markets. Financial planners now emphasize flexible withdrawal strategies, annuities, and TIPS ladders that adapt to real market conditions and inflation. This shift means your retirement strategy must be more dynamic and responsive than previous generations' static plans.

Additionally, pension availability continues declining while investment market volatility demands more sophisticated planning. The window for early retirement through aggressive saving has widened with access to tax-advantaged accounts like backdoor Roths and mega backdoor Roths, yet most people remain under-educated about these strategies. 2026 represents a pivotal moment when your retirement decisions compound into either security or stress.

The Science Behind Retirement

Retirement transitions trigger significant psychological shifts that research shows extend far beyond financial planning. Studies on the psychology of retirement reveal a predictable pattern: the 'honeymoon phase' immediately after leaving work brings excitement and freedom, typically lasting 6-12 months. During this period, people feel relief, adventure, and optimism as they explore life without work structure. However, the subsequent 'reorientation phase' often brings unexpected challenges—loss of identity, diminished sense of purpose, reduced social connections, and sometimes depression when the full reality of permanent life change becomes clear.

Psychological research identifies three core needs that predict successful retirement transitions: autonomy (freedom to design days aligned with personal values), competence (engaging in activities that challenge and develop skills), and relatedness (maintaining meaningful social connections). Retirees who satisfy all three needs report significantly higher life satisfaction than those who achieve financial security but neglect the psychological dimensions. The science reveals that a secure retirement requires more than money—it demands intentional relationship cultivation, meaningful activities, and purposeful engagement with life.

Retirement Transition Phases

Timeline showing emotional and psychological stages through early, middle, and late retirement

🔍 Click to enlarge

Key Components of Retirement

Tax-Advantaged Savings Accounts

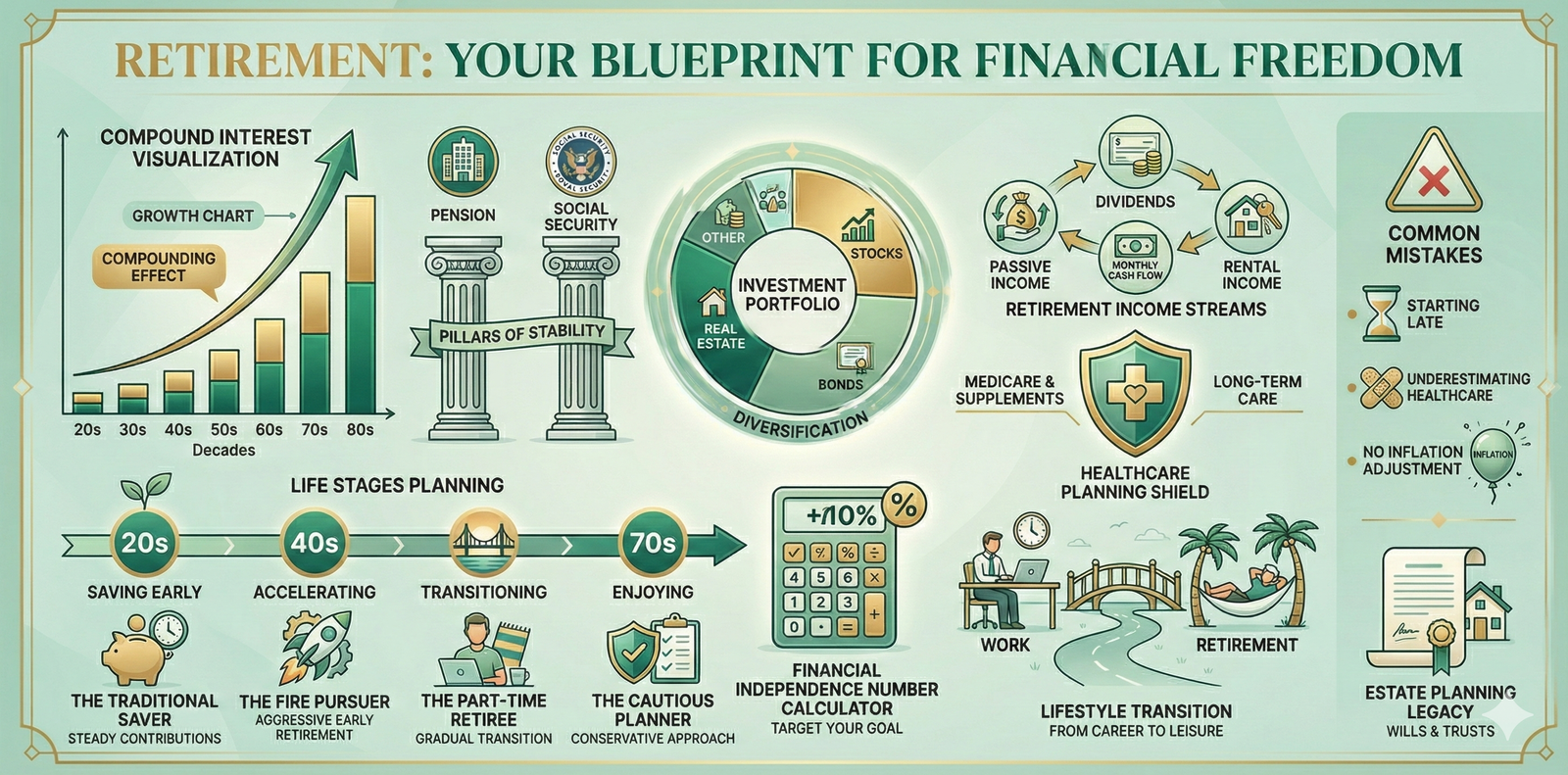

The foundation of retirement wealth typically rests on tax-advantaged accounts: 401(k)s, IRAs, and employer pensions. A 401(k) through your employer offers the advantage of potential matching contributions (free money) and higher annual contribution limits ($24,500 in 2026 for those under 50). Traditional 401(k)s reduce current taxable income, while Roth 401(k)s allow tax-free withdrawals in retirement. Individual Retirement Accounts (IRAs) provide flexibility—traditional IRAs offer immediate tax deductions while Roth IRAs deliver tax-free growth and withdrawals. For those with high incomes, strategies like backdoor Roths and mega backdoor Roths unlock significantly higher retirement savings capacity.

Investment Portfolio Strategy

Your investment approach fundamentally shapes retirement success. The traditional recommendation was aggressive investing while young, gradually shifting toward conservative bonds as retirement approaches. Modern research increasingly supports maintaining diversified stock exposure throughout retirement to combat inflation and extend portfolio longevity. The specific allocation depends on your risk tolerance, time horizon, and income needs. Most financial advisors recommend indexing (investing in low-cost index funds tracking market indices) rather than stock picking, as this approach reduces fees and outperforms 80% of managed portfolios over 15-year periods.

Income Planning and Withdrawal Strategy

How you withdraw money in retirement matters enormously. The outdated 4% rule—withdrawing 4% of your portfolio annually—no longer adequately accounts for market volatility and individual circumstances. Sophisticated retirees now use flexible withdrawal strategies that adjust based on market performance, inflation, and spending needs. Some use 'bucket strategies' where three years of spending remains in cash and bonds while longer-term funds invest for growth. Others employ annuities to cover essential expenses, providing peace of mind while allowing stock investments to address discretionary spending and legacy goals. Roth conversions before Medicare eligibility can reduce future Required Minimum Distributions while managing tax brackets strategically.

Social Security and Benefits Optimization

Social Security provides the only inflation-adjusted income source guaranteed for life, making optimization crucial. You can claim as early as age 62, but delaying until age 70 increases annual benefits by approximately 24% per year of delay—a return that's impossible to achieve through conservative investing. For married couples, coordinated claiming strategies can substantially increase lifetime benefits. Understanding your Full Retirement Age (67 for those born 1960 or later), calculating break-even ages, and considering longevity in your family create the foundation for optimal claiming decisions. Some people might benefit from claiming earlier to enjoy active retirement years; others choose delay for security and inflation protection.

| Account Type | Annual Contribution Limit | Tax Treatment |

|---|---|---|

| Traditional 401(k) | $24,500 | Pre-tax contributions, tax-deferred growth |

| Roth 401(k) | $24,500 | After-tax contributions, tax-free growth |

| Traditional IRA | $7,000 | Deductible contributions (if eligible), tax-deferred growth |

| Roth IRA | $7,000 | After-tax contributions, tax-free growth, no RMDs |

| HSA (Health Savings Account) | $4,300 individual | Triple tax advantage: deductible, grows tax-free, tax-free healthcare withdrawals |

How to Apply Retirement: Step by Step

- Step 1: Calculate your retirement number by identifying annual spending needs in retirement and multiplying by 25 (using the traditional 4% rule as baseline). For example, if you spend $60,000 annually, you'd target $1.5 million in savings.

- Step 2: Maximize your 401(k) contributions to at least capture any employer match, since matched contributions are immediate 50-100% returns on investment. If your employer matches dollar-for-dollar up to 6%, contribute at least 6%.

- Step 3: Open and contribute to an IRA—traditional for immediate tax deductions or Roth for tax-free growth. If you're over 50, take advantage of catch-up contributions of an additional $1,000 annually.

- Step 4: Build a diversified investment portfolio aligned with your risk tolerance, typically including 60-80% stocks and 20-40% bonds depending on your age and timeline. Use low-cost index funds as your foundation.

- Step 5: Implement a tax optimization strategy including annual Roth conversions if appropriate, tax-loss harvesting in taxable accounts, and strategic charitable giving through donor-advised funds.

- Step 6: Plan your Social Security claiming strategy by understanding your Full Retirement Age, break-even analysis between claiming early versus late, and coordinated strategies if married.

- Step 7: Create a flexible withdrawal plan that accounts for variable market returns, inflation, and changing needs—moving beyond simplistic percentage rules to responsive strategies.

- Step 8: Address healthcare coverage before Medicare eligibility (age 65), researching Affordable Care Act marketplace plans, COBRA continuation, or spousal coverage during early retirement years.

- Step 9: Develop a transition plan including what gives your retired life meaning (activities, relationships, learning, contribution), not just financial details.

- Step 10: Review and adjust your retirement plan annually, updating assumptions about life expectancy, market returns, spending patterns, and Social Security claiming as circumstances change.

Retirement Across Life Stages

Young Adulthood (18-35)

Your twenties and thirties represent retirement's most powerful decade because compound interest multiplies small contributions into substantial wealth. Someone who invests $500 monthly starting at age 25 will have $250,000+ by 65, assuming 7% annual returns. Yet this age group often neglects retirement, focusing instead on current expenses. The optimal strategy is automating contributions to your 401(k) and IRA immediately upon employment, treating retirement savings like non-negotiable bills. Even modest contributions—10-15% of income—compound into substantial freedom decades later. Additionally, these years offer the highest risk tolerance; stock-heavy portfolios can weather market volatility and recover during multiple business cycles before retirement.

Middle Adulthood (35-55)

During your peak earning years, retirement acceleration becomes possible. Income typically peaks, children may become more independent, and you can increase savings rates substantially. This phase offers the opportunity to shift from 'are we on track?' to 'how can we accelerate?' Strategies include maximizing employer benefits, exploring backdoor and mega backdoor Roth conversions, investing windfalls (bonuses, inheritances, stock options) directly to retirement accounts rather than spending, and potentially considering semi-retirement or career transitions that prioritize meaning over maximum income. Many people in this stage benefit from working with a fee-only financial planner to optimize complex tax situations and investment strategies. This is also when many face the challenge of balancing parental elder care costs with retirement savings, requiring intentional boundaries and planning.

Later Adulthood (55+)

As retirement approaches, strategy shifts toward preservation, tax optimization, and psychological preparation. Those age 50+ can make 'catch-up' contributions of $7,500 to 401(k)s and $1,000 to IRAs, accelerating final accumulation years. This phase involves detailed healthcare planning (understanding Medicare options, prescription drug coverage, supplemental insurance), Social Security optimization, and implementing withdrawal sequences that minimize taxes. Many people benefit from phased retirement—reducing hours or transitioning to consulting before full retirement—allowing adjustment to the identity shift while maintaining some structure and income. This is the critical period to cultivate retirement relationships and activities, ensuring you don't retire into isolation.

Profiles: Your Retirement Approach

The Traditional Saver

- Reliable income stability and employer 401(k) matching

- Long-term diversified investments with rebalancing discipline

- Healthcare planning for gap years before Medicare eligibility

Common pitfall: Retiring at the calendar date rather than when numbers actually support retirement, creating financial stress in later years

Best move: Model retirement using Monte Carlo simulations testing 1000+ market scenarios, ensuring 90%+ probability of success across various market conditions

The FIRE Pursuer

- Aggressive savings rate (50%+ of income) from high compensation

- Tax-efficient investment vehicles including backdoor Roths, mega backdoor Roths, and taxable investing

- Healthcare solution for decades before Medicare (often through ACA marketplace)

Common pitfall: Over-optimism about sustainable withdrawal rates, underestimating healthcare costs, or lifestyle inflation when income increases

Best move: Test early retirement with one-year trial maintaining typical spending while living off portfolio withdrawals, building confidence in your number

The Part-Time Retiree

- Phased transition combining part-time work income with portfolio withdrawals

- Flexible work arrangements (consulting, freelance, seasonal) that match lifestyle goals

- Healthcare through employer if part-time position provides coverage

Common pitfall: Part-time work consuming all free time, negating retirement's freedom benefits, or income pressure preventing genuine retirement mindset

Best move: Define specific hours for part-time work and protect remaining time fiercely for retirement activities, treating scheduled work hours as seriously as employment did

The Cautious Planner

- Conservative withdrawal strategies emphasizing capital preservation

- Substantial emergency funds and safe accounts for peace of mind

- Regular check-ins with financial advisor providing reassurance and adjustment

Common pitfall: Excessive conservatism resulting in under-spending retirement years due to inflation fears, living below actual means unnecessarily

Best move: Balance conservative accounts with growth accounts, spending from conservative sources while investments compound, achieving both security and flexibility

Common Retirement Mistakes

Many people underestimate healthcare costs in retirement, neglecting this largest expense category after housing and food. They budget for current medical spending while ignoring how dramatically costs escalate with age. A healthy 65-year-old couple should expect $550,000+ in total healthcare costs through age 85. This surprise often forces unwanted spending reductions or portfolio stress during peak medical-need years. Solution: explicitly budget healthcare into retirement plans, exploring long-term care insurance, and maintaining investment flexibility.

Another critical error involves poor Social Security timing decisions. Many people claim at 62 because they're retiring, failing to recognize that delayed claiming to 70 increases lifetime benefits by 76% for single filers. Someone who lives to 85 would claim $400,000+ additional benefits through delay versus early claiming. Yet claiming decisions often receive less planning attention than investment allocation. Solution: use Social Security break-even calculators and stress-test various scenarios based on family longevity patterns.

A third mistake involves retiring into isolation, losing work relationships without building retirement communities. This often contributes to depression, shortened lifespans, and diminished life satisfaction. The psychological transition requires intentional relationship building and meaningful activities, not automatic happiness from freedom. Solution: before retiring, identify specific communities you'll join (clubs, volunteer organizations, classes, religious groups) and schedule regular engagement.

Most Common Retirement Planning Errors

Showing frequency and impact of typical retirement mistakes

🔍 Click to enlarge

Science and Studies

Contemporary retirement research reveals that psychological preparation rivals financial planning in determining retirement satisfaction. Studies from the University of Washington and retirement transition psychology research consistently show that retirees who proactively cultivate meaning, maintain social connections, and establish identity beyond work report 30-40% higher life satisfaction than financially secure retirees who neglect these dimensions. Financial security is necessary but insufficient for thriving retirement.

- Fidelity's 2026 Retirement Planning Research: Tax-advantaged catch-up contributions for those over 50 demonstrate that accelerated saving in final working years can extend retirement timeline by 3-5 years and reduce required savings rates.

- Social Security Administration Analysis: Couples who delay claiming one partner's benefits to age 70 while the other claims at Full Retirement Age increase household lifetime benefits by $50,000-$100,000+ compared to early claiming strategies.

- Healthcare Cost Study (RAND Corporation): Healthcare costs for average retiring couple now exceed $550,000 through age 85, representing the largest unplanned expense surprise in retirement and requiring explicit budgeting.

- Investment Withdrawal Research: Flexible withdrawal strategies that adjust based on market conditions outperform fixed percentage withdrawals, with success rates increasing from 75% (4% rule) to 85-90% under dynamic strategies.

- Retirement Transition Psychology (UW Retirement Association): The 'honeymoon-reorientation-stabilization' model predicted retirement satisfaction with 85% accuracy; retirees who anticipated the reorientation phase adjusted successfully with 2x higher satisfaction than those surprised by emotional changes.

Your First Micro Habit

Start Small Today

Today's action: Spend 15 minutes reviewing your current retirement savings: add up all 401(k)s, IRAs, and investment accounts, then calculate how many years of expenses this represents (divide total by annual spending need). Write the number down—this baseline awareness shifts vague worry into concrete motivation.

Most people avoid calculating their retirement reality because ignorance feels safer than facing gaps. One honest number transforms retirement from abstract future stress into actionable present planning. This single calculation often motivates increased saving, optimization research, or professional guidance—powerful change from mere awareness.

Track your retirement progress and get personalized AI coaching with our app.

Quick Assessment

What is your current relationship with retirement planning?

Your current stage determines which retirement strategies matter most. Early savers need aggressive growth; steady savers need optimization; confident savers need lifestyle planning.

What's your most pressing retirement concern?

Your primary concern reveals your next priority action. Most people need multiple strategies, but addressing your specific concern first builds momentum.

How far are you from your ideal retirement date?

Timeline determines strategy urgency and acceptable risk. Near-term retirees need income planning; long-term savers should prioritize growth and tax optimization.

Take our full assessment to get personalized recommendations.

Discover Your Style →Next Steps

Your retirement begins with clarity: understanding exactly where you stand financially and psychologically. Complete the micro habit above—calculate your retirement number and current progress. This single action transforms retirement from vague anxiety into concrete planning. Next, identify your next immediate action based on your life stage: those early in careers should prioritize consistent saving and avoiding debt; mid-career professionals should optimize tax strategies and increase savings rate; those approaching retirement should validate numbers and address healthcare planning. All should work on non-financial retirement dimensions simultaneously—exploring what brings meaning, building communities you'll join, and preparing for the identity transition.

Consider working with a fee-only financial advisor if your situation involves complexity, substantial assets, or significant uncertainty. However, many people benefit first from reading comprehensive resources, using retirement calculators, and beginning implementation independently. The best financial plan is one you understand and will actually follow. Retirement represents freedom earned through decades of choices—make your current choices align with the future you're building.

Get personalized guidance with AI coaching.

Start Your Journey →Research Sources

This article is based on peer-reviewed research and authoritative sources. Below are the key references we consulted:

Related Glossary Articles

Frequently Asked Questions

How much money do I need to retire?

A common rule is having 25x your annual expenses, based on the 4% withdrawal rule—though modern research suggests flexible withdrawal strategies might allow lower amounts. If you spend $60,000 annually, target $1.5 million as a baseline. However, individual circumstances vary: high healthcare costs, expensive hobbies, or family support needs increase your number; low expenses or early Social Security decrease it. Use retirement calculators to model your specific situation.

Should I retire early or work longer?

The optimal decision depends on your financial security, health, career satisfaction, and what gives your life meaning. Research shows that working in jobs you find meaningful extends longevity and life satisfaction, while forced early retirement sometimes decreases both. However, if you're burned out or have limited years of health remaining, early retirement maximizes their enjoyment. Calculate whether your savings support early retirement without excessive lifestyle restriction, then decide based on wellbeing, not just money.

What happens to my health insurance before Medicare at 65?

Early retirees have several options: Affordable Care Act (ACA) marketplace plans (potentially subsidized based on income), COBRA continuation from your employer (expensive but comprehensive), spousal coverage if your partner still works, or part-time work providing employer benefits. Healthcare costs often surprise early retirees—budget $400-800 monthly per person. Understanding these options before retiring prevents coverage gaps and unexpected expenses.

Can I retire earlier through aggressive saving (FIRE)?

Yes—people achieving 70%+ savings rates can retire decades early, with some reaching financial independence in their 30s-40s. However, FIRE requires exceptional discipline, sufficient income to save that much, and strategic tax planning including backdoor Roths and mega backdoor Roths. It's possible but demands commitment beyond typical retirement planning. Test the feasibility with your income, expenses, and long-term health needs.

What's the best retirement investment strategy?

Research consistently shows that low-cost, diversified index funds outperform 80% of actively managed portfolios over 15+ years. A simple approach: 80% total stock market index, 20% international stocks, rebalancing annually. As you near retirement, gradually increase bond allocation, but maintain stock exposure to combat inflation. Avoid frequent trading, market timing, or concentrated positions. Simplicity and consistency often beat complexity and optimization in retirement investing.

Take the Next Step

Ready to improve your wellbeing? Take our free assessment to get personalized recommendations based on your unique situation.

- Discover your strengths and gaps

- Get personalized quick wins

- Track your progress over time

- Evidence-based strategies