Investment Estrategias

Building wealth is one of the most important financial goals you can set for yourself. Yet many people feel overwhelmed by the complexity of investing, uncertain about where to start, or afraid of making costly mistakes. The truth is that successful investing doesn't require complex strategies or insider knowledge—it requires understanding proven principles and developing a clear plan aligned with your goals. Whether you're starting with your first investment or looking to optimize an existing portfolio, the right investment strategies can transform your financial future. This guide reveals actionable approaches used by successful investors worldwide, helping you make confident decisions about your money.

Investment strategies are not one-size-fits-all frameworks. They adapt to your life stage, financial situation, risk tolerance, and long-term goals. What works for a 25-year-old building their first portfolio differs significantly from what a 55-year-old approaching retirement needs.

Understanding core investment principles helps you navigate market fluctuations with calm certainty, reduce costly emotional decisions, and build systematic wealth over time.

What Is Investment Strategies?

Investment strategies are structured approaches to making decisions about where and how to deploy your money with the goal of building wealth over time. A strategy encompasses your overall plan—which asset classes to invest in, how much to allocate to each, how frequently to invest, when to rebalance, and how to respond to market changes. Rather than making random stock picks or following hot tips, a genuine investment strategy is a personalized roadmap based on your specific circumstances, time horizon, and risk tolerance.

Not medical advice.

Investment strategies have evolved significantly over the past century, from early buy-and-hold approaches to modern sophisticated frameworks that leverage data and behavioral psychology. Today's most effective strategies combine time-tested principles with current research, creating flexible systems that work through different market conditions. The strategies that serve you best are those you can stick with consistently, regardless of market headlines or peer pressure.

Surprising Insight: Surprising Insight: Studies show that the average investor underperforms their own investments by 1-3% annually due to emotional decision-making—not because their strategy was flawed, but because they abandoned it during market downturns.

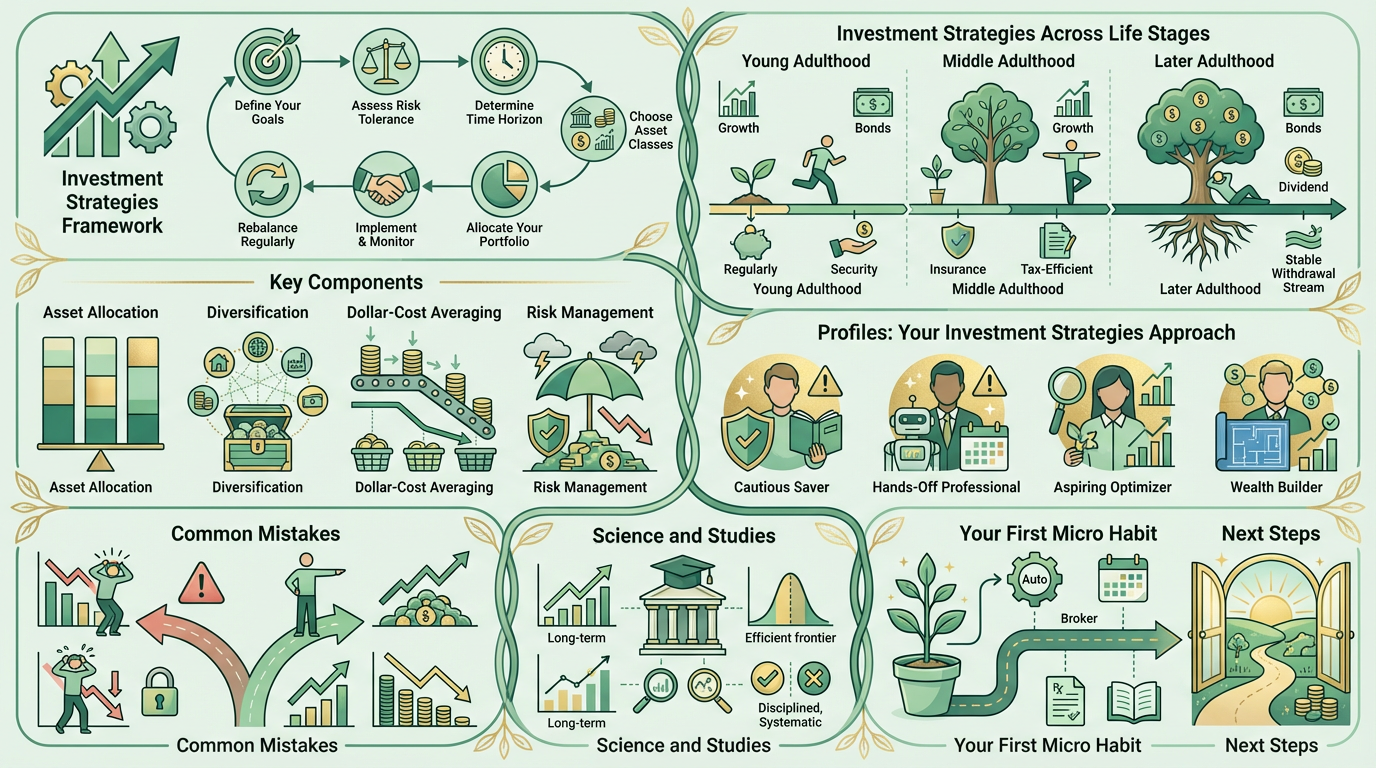

Investment Strategy Framework

Visual representation showing how investment strategies connect goals, risk tolerance, time horizon, and asset allocation into a cohesive plan

🔍 Click to enlarge

Why Investment Strategies Matter in 2026

The investment landscape in 2026 presents both unprecedented opportunities and unique challenges. Interest rates, inflation, geopolitical tensions, and technological disruption create a complex environment where random investing often leads to poor outcomes. Having a deliberate strategy acts as your financial compass, helping you navigate volatility with confidence rather than panic. Strategic investing separates those who build lasting wealth from those who remain perpetually stressed about money. Your strategy becomes your trusted decision-making framework that guides you through uncertainty and doubt.

Market volatility is higher than ever, with major indices experiencing 10-15% swings within months. Without a clear strategy, these movements trigger emotional responses—selling after drops, chasing winners after rallies—that lock in losses and miss gains. Strategic investors view volatility as opportunity, maintaining discipline through understanding that downturns are temporary and recoveries are inevitable. Historical data demonstrates that every market crash from 1926 to today has been followed by new all-time highs within years. Those who stayed invested during crashes captured the subsequent recoveries. Those who sold at market lows watched from the sidelines as wealth was rebuilt.

The democratization of investing means you can now access professional-grade tools, low-cost index funds, and fractional shares with minimal capital. Young adults can begin with $50, middle-aged professionals can automate investments painlessly, and those nearing retirement can optimize tax efficiency. Yet this accessibility creates analysis paralysis unless you have a clear strategy guiding your decisions. Too many people spend weeks researching investment options yet never invest a dollar. Investment strategies ensure you're taking full advantage of these tools in ways that serve your specific situation. Your strategy converts analysis into action, hesitation into consistency, and confusion into clarity.

The 2026 economic environment rewards disciplined investors more than ever. Those following systematic strategies benefit from market dislocations that panic-driven investors create. When headlines scream danger and crowds flee to cash, strategic investors following their plan are buying quality investments at substantial discounts. This contrarian positioning—buying when others fear—is what creates generational wealth. Your investment strategy is your psychological insurance policy against succumbing to crowd psychology.

The Science Behind Investment Strategies

Decades of academic research from institutions like Harvard Business School, Stanford Graduate School of Business, and MIT have yielded consistent findings about what works in investing. Nobel Prize-winning economist Harry Markowitz demonstrated that portfolio diversification reduces risk without sacrificing returns. His efficient frontier concept shows that the optimal portfolio isn't necessarily the one with highest potential returns, but rather the one with the best risk-adjusted returns—the most return per unit of risk taken. This revolutionary insight—that adding lower-returning assets can improve overall portfolio performance through diversification—fundamentally changed how professional investors approach portfolio construction worldwide.

Behavioral finance research reveals why most investors underperform. Cognitive biases like loss aversion (fearing losses twice as much as gains), recency bias (overweighting recent events), and herd behavior (following the crowd) consistently lead to poor timing decisions. Systematic investment strategies combat these biases by removing emotion and replacing it with predetermined rules. Research shows that investors who follow disciplined strategies consistently outperform those who make ad-hoc decisions, regardless of market conditions. A study by Vanguard found that the gap between a disciplined investor following a strategy and an emotional investor abandoning plans during downturns often exceeds 2% annually—translating to hundreds of thousands of dollars over decades.

The concept of rebalancing, where investors sell appreciating assets to buy depreciating ones, seems counterintuitive yet produces measurable outperformance. This systematic approach forces investors to buy low and sell high automatically, without requiring the emotional strength to act against crowd sentiment. Historical research tracking portfolios from 1926 through 2024 shows that rebalancing annually adds approximately 0.5% to returns while reducing portfolio volatility by 15-20%. This risk-reduction benefit alone makes disciplined rebalancing worthwhile for long-term investors seeking sustainable wealth building without excessive portfolio swings.

Modern portfolio theory teaches that systematic risk (market-wide movements) cannot be eliminated but unsystematic risk (individual security problems) can be diversified away. This distinction matters enormously. An investor holding only three stocks bears both types of risk. The same investor holding a diversified portfolio of 100+ stocks through index funds eliminates unsystematic risk while keeping systematic risk exposure. Why accept unnecessary risk from individual stock failures when diversification painlessly removes it? This scientific principle explains why 90% of professional investors now recommend diversified index funds for most investors.

Risk vs. Return Relationship

Visualization showing how different asset allocations create different risk-return profiles, demonstrating the efficient frontier concept

🔍 Click to enlarge

Key Components of Investment Strategies

Asset Allocation

Asset allocation—deciding what percentage of your portfolio to invest in stocks, bonds, cash, and alternatives—is your single most important decision. Research shows that 90% of portfolio performance variation comes from your asset allocation choice, not from which specific stocks you pick. A balanced investor might hold 60% stocks and 40% bonds. A younger investor with higher risk tolerance might choose 80% stocks and 20% bonds. An older investor nearing retirement might prefer 40% stocks and 60% bonds. Your allocation depends on your age, time horizon, income stability, and personal comfort with volatility. The right allocation is one you can maintain through market cycles without panicking. Think of asset allocation as your portfolio's fundamental structure—the basic architecture upon which everything else is built. A poorly chosen allocation creates perpetual stress regardless of how sophisticated your stock selection becomes.

To determine appropriate allocation, consider several factors. Your time horizon—years until you need this money—most directly affects your stock percentage. Someone investing for retirement 40 years away can afford to accept stock market volatility knowing decades remain for recovery. Someone needing funds within two years must emphasize stability. Your income stability also matters. A tenured professor can handle portfolio volatility because income is secure. A freelancer with uncertain income should maintain larger reserve of stable bonds. Your risk capacity (ability to handle losses without lifestyle impact) differs from risk tolerance (comfort with volatility). A millionaire can tolerate portfolio drops better than someone living paycheck-to-paycheck, regardless of psychological comfort levels.

Diversification

Diversification means spreading your investments across different asset classes, sectors, and geographies so that poor performance in one area doesn't devastate your entire portfolio. When you own only technology stocks and the tech sector declines, your entire portfolio suffers. But if you own technology, healthcare, industrials, consumer goods, and energy stocks across multiple countries, a downturn in any single area has limited impact. True diversification extends beyond stocks—holding bonds, real estate, and other assets that move differently than stocks creates more stable returns. Financial institutions and successful long-term investors all emphasize diversification as the closest thing to a free lunch in investing. Unlike other investment benefits requiring higher risk or lower fees, diversification increases returns while actually reducing risk.

Effective diversification requires understanding correlation—how different investments move together. Stocks and bonds historically move in opposite directions, particularly during economic downturns. When stock prices crash, bond prices typically rise, cushioning portfolio losses. Adding bonds doesn't reduce returns as much as naive investors expect because they capture appreciation during stock market declines. This relationship changes periodically—stagflation of the 1970s saw both stocks and bonds decline simultaneously. But across long-term periods, diversification has consistently reduced volatility while maintaining reasonable returns. The magic of diversification is that adding something that returns less (bonds) actually improves overall portfolio performance through risk reduction.

Geographic diversification adds another layer of protection. A portfolio holding only U.S. stocks faces U.S.-specific risks—regulatory changes, economic slowdown, market overvaluation. International exposure reduces concentration. When developed markets underperform, emerging markets may outperform, balancing overall returns. While international investing adds currency risk (exchange rate fluctuations), most financial advisors recommend 20-30% of equity allocation in developed international markets and small exposure to emerging markets. This geographic spread ensures that your portfolio benefits from growth wherever it occurs globally, rather than betting entirely on U.S. performance.

Dollar-Cost Averaging

Dollar-cost averaging (DCA) means investing a fixed amount at regular intervals—such as $500 every month—regardless of whether markets are rising or falling. This approach removes the pressure to time the market perfectly because you're investing continuously. When prices are high, your fixed investment buys fewer shares. When prices are low, your fixed investment buys more shares. Over time, you buy shares at an average cost lower than the average price. DCA is psychologically powerful because it maintains discipline during both market peaks and crashes, making it ideal for busy professionals and young savers who can't or shouldn't try to time markets. This simple mechanism automatically implements the buy-low, sell-high philosophy that most investors understand intellectually but struggle to execute emotionally.

Consider a concrete example illustrating DCA benefits. An investor commits to buying $1,000 monthly of a mutual fund. In January, the fund trades at $100, purchasing ten shares. In February, market decline drops the price to $80, purchasing twelve-point-five shares. In March, recovery brings price to $90, purchasing eleven-point-one shares. Over three months, thirty-three-point-six shares were purchased at average cost of ninety dollars per share. The fund's price averaged ninety-three dollars across the period, yet this investor bought at effective cost below market average. This happens automatically without requiring market timing expertise or luck. The periodic investment discipline creates mathematical advantage that compounds over decades.

DCA particularly benefits younger investors building from zero assets. Monthly contributions of even $100-200 create powerful discipline while avoiding the paralysis of timing market entry perfectly. Waiting for the 'right price' often means never investing at all. DCA eliminates this hesitation—you invest mechanically, building wealth systematically regardless of current valuations. While lump-sum investing theoretically outperforms DCA in rising markets (since all money compounds for longer), DCA's psychological benefits often exceed this theoretical advantage. An investor who stays invested via DCA beats a theoretically-better investor who quits during volatility and misses recovery gains.

Risk Management

Risk management in investing means understanding the specific risks you're taking and deliberately limiting them. This includes concentration risk (putting too much in one investment), leverage risk (borrowing to invest), timing risk (investing everything at market peaks), and unsystematic risk (sector or company-specific problems). Effective risk management strategies include position sizing (never letting one position become too large), rebalancing (selling winners and buying losers to maintain your target allocation), and maintaining an emergency fund separate from investments. Protecting your capital from catastrophic losses is as important as pursuing gains. Professional investors spend as much time managing risk as chasing returns—recognizing that capital preservation enables future compounding while losses destroy it.

Concentration risk represents the single largest preventable mistake amateur investors make. Putting significant money in a few stocks or into employer stock often feels acceptable when holdings are doing well. But this concentrated risk explodes during downturns affecting those specific companies or sectors. Consider the technology stock disaster of 2022 where concentrated tech investors lost 30-50% while diversified investors experienced 15-20% declines. Or employees holding too much in employer stock (Enron, Lehman Brothers) who lost both jobs and retirement savings simultaneously. Position sizing discipline prevents catastrophe. A common rule: never let any single position exceed 5% of portfolio or more than you could stomach losing. This simple constraint prevents concentration risk that could derail your entire financial plan.

Leverage (borrowing to invest) magnifies both gains and losses dangerously. Investors who borrow money to buy stocks double their risk. A 20% market decline becomes 40% portfolio loss when leveraged. Historically, highly leveraged investors often face margin calls—forced liquidation at terrible prices during crashes. Protecting yourself requires avoiding leverage except in specific professional contexts where you fully understand consequences. Your personal investment strategy should assume you'll hold through downturns. Leverage forces you to sell at market lows, the exact opposite of what your strategy requires. The wealthiest long-term investors built wealth without leverage, proving it unnecessary for successful investing.

| Strategy | Time Commitment | Best For | Key Advantage |

|---|---|---|---|

| Buy and Hold | Minimal | Long-term investors | Simple, low-cost, tax-efficient |

| Dollar-Cost Averaging | Low | Regular savers | Removes timing pressure |

| Value Investing | High | Active investors | Buying undervalued assets |

| Growth Investing | High | Younger investors | Capitalizing on expansion |

| Index Investing | Minimal | Hands-off investors | Broad diversification, low fees |

| Tactical Allocation | High | Experienced investors | Adapting to market conditions |

How to Apply Investment Strategies: Step by Step

- Step 1: Define your investment goals—whether building wealth, saving for retirement, down payments, or education. Be specific about amounts and timelines.

- Step 2: Calculate your risk tolerance by honestly assessing how you felt during past market corrections and what percentage declines you can withstand without panicking.

- Step 3: Determine your time horizon—the years until you need this money. Longer horizons allow more stock exposure; shorter horizons require more conservative allocations.

- Step 4: Choose your asset classes based on your allocation decision. Most beginning investors start with stocks, bonds, and cash or cash equivalents.

- Step 5: Select specific investments within each asset class, preferring low-cost index funds and ETFs that provide instant diversification and minimal fees.

- Step 6: Set up automated investing through your employer's 401(k) plan or by scheduling monthly transfers to your brokerage account, removing the willpower requirement.

- Step 7: Monitor your portfolio quarterly, reviewing performance without obsessing over daily fluctuations or making emotional changes to your strategy.

- Step 8: Rebalance annually or when your allocation drifts more than 5-10% from your target, selling winners and buying losers to maintain discipline.

- Step 9: Track your progress against your goals rather than against market indices or others' portfolios, remembering that different people have different objectives.

- Step 10: Adjust your strategy as your life circumstances change—marriage, children, job changes, approaching retirement—keeping your approach aligned with current reality.

Investment Strategies Across Life Stages

Adultez joven (18-35)

Your greatest advantage during young adulthood is time. Decades of compound growth ahead mean you can afford to take more investment risk and recover from market downturns. Recommended allocation: 80-90% stocks, 10-20% bonds. Focus on maximizing contributions to retirement accounts—especially employer-matching 401(k) plans, which are guaranteed returns on your money. Automate everything so you invest consistently without thinking about it. If the stock market crashes during these years, celebrate because your investments are on sale. Ignore market noise and stay focused on consistently adding money to your investments. Starting early with even small amounts ($50-100 monthly) creates enormous wealth through compound growth over 40+ years.

Edad media (35-55)

Middle adulthood brings the intersection of peak earning years and growing financial responsibilities. Recommended allocation: 60-75% stocks, 25-40% bonds. You've built some wealth but can't afford major mistakes. Maintain aggressive growth orientation while introducing bonds to reduce portfolio volatility. Ensure your insurance coverage (life, disability, health) protects your family if you can't work. Consider tax-efficient strategies—tax-loss harvesting, maximizing retirement account contributions, strategic charitable giving. Rebalance annually to maintain your target allocation. Review your strategy when major life events occur: inheritance, bonuses, career changes, or children's education funding needs. Middle-aged investors often have the resources to implement sophisticated strategies but must resist lifestyle inflation that prevents wealth accumulation.

Adultez tardía (55+)

As you approach and enter retirement, preservation becomes more important than growth. Recommended allocation: 40-60% stocks, 40-60% bonds, depending on your retirement timeline. Shift toward a focus on generating income and maintaining purchasing power. At 55, if you retire at 65, you still have 30+ years until age 95, so you can't abandon stocks entirely. However, emphasize stability over growth. Consider laddered bond portfolios that mature at different times, creating regular income. Ensure your portfolio can sustain 4% annual withdrawals (adjusted for inflation) without running out of money. Take advantage of catch-up contributions to retirement accounts. Review your portfolio annually and rebalance, but avoid making dramatic changes based on current market conditions. Work with a financial professional to optimize Social Security claiming, minimize taxes, and structure distributions efficiently.

Profiles: Your Investment Strategies Approach

The Cautious Saver

- Clear step-by-step guidance without jargon

- Reassurance that slow, steady investing beats panic-selling

- Simple allocation focused on bonds and diversified funds

Common pitfall: Keeping too much in cash due to fear, missing decades of growth and failing to reach financial goals

Best move: Start with 60% bonds/40% stocks, automate contributions, and commit to not checking the portfolio more than quarterly to reduce anxiety

The Hands-Off Professional

- Minimal time commitment with maximum diversification

- Automated systems requiring no active management

- Clear rebalancing schedule

Common pitfall: Setting up investments initially but then ignoring them for years, allowing allocations to drift completely off-target

Best move: Use target-date funds or robo-advisors that automatically rebalance, set calendar reminders for annual reviews, and delegate management when possible

The Aspiring Optimizer

- Education about picking individual investments wisely

- Tools for analyzing performance and tax efficiency

- Strategies for beating index returns through active management

Common pitfall: Overtrading, excessive research, and overestimating ability to pick winners while incurring high costs and creating tax inefficiency

Best move: Limit portfolio to 20-30 holdings, rebalance annually rather than constantly, and measure results against low-cost benchmarks honestly over 5+ year periods

The Wealth Builder

- Comprehensive strategies for multiple financial goals simultaneously

- Advanced techniques like tax-loss harvesting and strategic asset location

- Integration with overall financial planning

Common pitfall: Pursuing complex strategies that create unnecessary costs, complexity, and regulatory issues without meaningful benefit

Best move: Maintain core index portfolio as foundation, use advanced strategies selectively only where they add clear value, and engage professional guidance for complexity

Common Investment Strategies Mistakes

The most prevalent mistake investors make is emotional decision-making during market volatility. When the stock market drops 20%, fear triggers selling at precisely the worst time—locking in losses right before the inevitable recovery. Successful investors recognize these emotions and follow their predetermined strategy instead. Market crashes are not reasons to abandon your plan; they're buying opportunities to acquire investments at discount prices. The investors who panicked and sold during the 2008 financial crisis missed the 400%+ gains from 2009-2020. Keep your strategy written down and review it when you feel tempted to change it. This simple practice prevents costly emotional decisions.

Another critical mistake is inadequate diversification or excessive concentration. Investors who own only technology stocks, only one company's stock, or only stocks from one country face catastrophic risk. When their concentrated area underperforms, their entire portfolio suffers. True diversification means holding stocks and bonds across different sectors, geographies, and asset classes so that downturns in any area have limited overall impact. Starting with index funds that hold hundreds of companies provides instant diversification and removes the burden of researching individual investments.

A third mistake is underestimating the impact of fees and costs. An investor who pays 1% annually in fees versus 0.1% for an index fund loses 10% of total returns over 30 years. That percentage difference translates to tens of thousands of dollars for a typical portfolio. Avoid actively-managed funds with high fees unless strong evidence supports that their picks beat the market after fees (spoiler: most don't). Use low-cost index funds and ETFs as your foundation, and if you use active management, limit it to where you have genuine competitive advantage or expertise.

Common Mistakes and Recovery Paths

Flowchart showing how common investment mistakes happen and how to recover from them with a strong strategy

🔍 Click to enlarge

Ciencia y estudios

Research from leading financial institutions consistently validates that disciplined, diversified investment strategies outperform emotional or reactive approaches. Studies examining institutional investors show that those following defined strategies achieve superior risk-adjusted returns compared to those making ad-hoc decisions. Academic research on dollar-cost averaging demonstrates its effectiveness in reducing average purchase costs and emotional decision-making. Analysis of the efficient frontier shows that optimal portfolios balance risk and return through diversification rather than betting heavily on single assets or sectors. Decades of empirical evidence demonstrate that investment strategy quality strongly correlates with financial success.

A landmark study by researchers at Carnegie Mellon University examined investment performance of over 35,000 individual investors from 1991 to 1996. Results revealed that investors making frequent trades underperformed buy-and-hold investors by 6.5% annually. The worst performers—those trading monthly—underperformed by over 8% yearly. This overtrading disadvantage comes from multiple sources: transaction costs, taxes on frequent trading, poor market timing instincts, and behavior-biased decisions. The study's implications are clear—most investors improve returns simply by trading less and sticking to strategy more consistently.

Another important analysis by Dimensional Fund Advisors examined performance from 1926-2024, spanning thirteen different bear markets and numerous crashes. Results showed that 90% of portfolio performance variance came from asset allocation, not security selection or market timing. Investors who maintained strategic allocations and rebalanced through crashes achieved superior long-term returns compared to those chasing better opportunities. This century-plus dataset removes any doubt about whether strategic discipline outperforms tactical improvisation.

- MIT School of Distance Learning (2025): Smart investment strategies for beginners emphasize systematic approaches over market timing, with documented outperformance from disciplined investors over decades.

- Vanguard Research (2024): Long-term studies show that buy-and-hold diversified portfolios beat active trading strategies 85% of the time, even among experienced investors with sophisticated tools.

- Investor.gov (SEC Resource): Beginner's guides to asset allocation, diversification, and rebalancing confirm that these foundational concepts drive long-term wealth creation and portfolio stability.

- Morgan Stanley Wealth Management (2023): Analysis of 1,000+ historical scenarios shows dollar-cost averaging reduces timing risk, though lump-sum investing performs better in rising markets overall.

- Harvard Business School (2025): Research on heterogeneous investor beliefs explains performance gaps between sophisticated and novice investors, highlighting the value of strategic planning and discipline.

Tu primer micro hábito

Comienza pequeño hoy

Today's action: Set up one automatic monthly investment into a diversified index fund (such as an S&P 500 fund or target-date fund) for at least $50. Let it run without checking it for three months to build confidence.

Automation removes decision-making friction, ensuring consistency regardless of your emotions or market conditions. Starting small removes the pressure of making a perfect decision, building confidence as you watch your account grow. The three-month delay trains you to ignore short-term market noise and focus on long-term goals. This simple action activates compound growth that multiplies over decades.

Track your micro habits and get personalized AI coaching with our app.

Evaluación rápida

How do you typically respond when investments drop 10-15% in value?

Your response reveals your true risk tolerance. Panickers need more bonds and smaller positions. Trusters are aligned for growth. Opportunistic investors need discipline to avoid overconfidence. Frequent checkers need stricter rules about when they're allowed to review.

What timeline do you have before needing this money?

Time horizon is crucial for allocation. Short timelines require conservative strategies protecting capital. Medium timelines allow balanced approaches. Long timelines enable aggressive growth since crashes have time to recover.

Which investment approach appeals to you most?

Your preference reveals the strategy you'll actually maintain. The best strategy is one you'll stick with, not necessarily the theoretically optimal one. Match your approach to your personality for sustainable wealth-building.

Take our full assessment to get personalized recommendations.

Discover Your Style →Preguntas frecuentes

Próximos pasos

Begin by choosing a broker that aligns with your approach. If you prefer simplicity, consider robo-advisors like Betterment, Vanguard Personal Advisor Services, or Wealthfront that automate your entire strategy. These services typically charge 0.25-0.50% annually for complete management. If you prefer more control, standard brokers like Fidelity, Charles Schwab, or Vanguard offer excellent tools and customer service. Most brokers charge no commissions on stocks and funds now, so focus on finding one with low fund fees and intuitive user experience. Research shows broker choice matters less than strategy consistency—choose and stick with it rather than constantly switching seeking perfection.

Next, define your personal investment allocation based on your time horizon and risk tolerance using this framework: your age plus 10 should be roughly the percentage in bonds (a 30-year-old might hold 40% bonds, a 50-year-old might hold 60% bonds). Or use simpler target-date funds that automatically adjust allocation as you age. Set up automatic monthly contributions that you barely notice—even $50-100 monthly compounds substantially over decades. Most brokers offer free automated transfers, removing behavioral friction that prevents consistent investing. The moment you set up automation, you've accomplished most of the hard work. From then on, your strategy runs itself.

After choosing your broker and setting up automation, take thirty minutes to write down your investment strategy. Document your target allocation, how frequently you'll rebalance (annually is standard), your time horizon, your reasons for this approach, and what market conditions would cause you to deviate from the plan. Keep this document accessible and reread it whenever market headlines tempt you to make emotional changes. This simple practice of writing down and reviewing your strategy separates successful long-term investors from those perpetually second-guessing themselves.

Finally, educate yourself but set boundaries on research. Reading two good books about investing (recommended: 'A Random Walk Down Wall Street' and 'The Intelligent Investor') will teach you more than 99% of investors know. Reading financial blogs and news daily usually hurts rather than helps, overwhelming you with short-term information that triggers emotional decisions. Establish information boundaries—perhaps monthly review of your portfolio—that align with your strategy rather than creating constant noise and temptation to tinker.

Get personalized guidance with AI coaching.

Start Your Journey →Research Sources

This article is based on peer-reviewed research and authoritative sources. Below are the key references we consulted:

Related Glossary Articles

Frequently Asked Questions

How much money do I need to start investing?

You can start with as little as $50-100 through most brokers today. Many employers offer 401(k) plans where you can contribute a percentage of each paycheck, often with matching free money. Fractional shares allow small dollar amounts to buy partial shares of any stock or fund. The amount matters less than consistency and starting early; even small amounts grow significantly over decades.

Should I invest a lump sum or use dollar-cost averaging?

Research shows lump-sum investing performs better statistically in rising markets (since money compounds longer), but dollar-cost averaging reduces emotional stress and timing risk for most people. If you have cash available now and strong conviction, lump-sum works. If you want to avoid the stress of trying to time the market perfectly, dollar-cost averaging is more sustainable. The research also shows that people using DCA stay invested through downturns while lump-sum investors often panic-sell during crashes, negating the theoretical advantage. The best strategy is one you'll actually execute consistently. Automate monthly investments and stop worrying about timing.

How often should I check my portfolio?

Quarterly reviews are healthy for monitoring progress toward goals. Annual rebalancing maintains your target allocation. Anything more frequent usually triggers emotional decisions that harm returns. Set a calendar reminder for your quarterly and annual reviews, then deliberately avoid checking prices between them. Remember: you're not trying to beat the market short-term; you're trying to reach your long-term goals.

Is it possible to beat the market with individual stock picking?

Data shows that 85-90% of professional fund managers fail to beat low-cost index funds over 15+ year periods, especially after fees. If professionals can't beat the market consistently, individual investors statistically can't either. The rare investors who beat the market either get lucky or have genuine competitive advantages (professional economists, industry expertise, etc.). For most people, index funds are the smarter choice financially and psychologically.

What should I do when the market crashes?

Market crashes are temporary dips followed by recovery to new highs. History shows this pattern repeating across all crashes, from 1987 to 2008 to 2020. Your strategy assumes crashes will happen and remain invested through them. In fact, crashes are buying opportunities—your ongoing contributions buy investments at discounted prices. The worst decision is selling during crashes, locking in losses. The best decision is staying calm, remembering your plan, and continuing to invest.

Take the Next Step

Ready to improve your wellbeing? Take our free assessment to get personalized recommendations based on your unique situation.

- Discover your strengths and gaps

- Get personalized quick wins

- Track your progress over time

- Evidence-based strategies